There is quite a bit of literature that the market is inherently volatile, punctuated by moments of seeming predictability. However, when viewed from a macro perspective spanning years, the market actually has predictable broad trends. That does not mean this volatility is inherently bad. In fact, these periods of volatility should be viewed as opportunities.

We embrace this volatility and adapt to it. What we recognise as volatility is the aggregated result of people being emotional and tied to sentiment, their hopes, their panic, their optimism, moving the market as an overreaction to events and trends. Sometimes this is the result of manipulation, even by state players, on a massive scale. At other times, it is the result of people seeing something in a news clip on a related counter, something on a very small scale.

We ride the swells of this volatility by keeping to a few principles. We look for well-run companies, with good market fundamentals. The numbers do not lie, unless you are looking at them in the wrong context. We consider where these companies are positioned, and pay more attention to where they are going, and not invest on the basis of legacy. That is sentiment, and sentiment is an emotional connection, not a reality of the company position.

This is where investing over an extended investment horizon really works. What we are doing is utilising the magic of compounding. This is what real investment actually is. People trying to spot a bargain, or following a hot tip are not investors. They are gamblers. Often, they are leveraged, which means they are utilising compounding the wrong way. Compounding works for the investor when it is about taking and holding a well-researched position over an extended period, letting the compounded interest of the stock generate growth. A speculator, on the other hand, is borrowing, and compounded borrowings are a quick way to lose money.

Because of this compounding effect, the best time to take a position is often when the market is down, replete with bad news. Due to market sentiment, even good stocks are undervalued. The trick is sniffing out gold from the dross in all that. There is a method to this, and it based on logic.

Firstly, we identify growth industries. For example, in a pandemic economy, we expect growth in online retail, technology, and healthcare. It does not take a genius to figure that out. In certain markets, we all consider light manufacturing, because somebody has to make all that protective equipment, gloves and masks. And obviously, the stock with the greatest growth would be pharmaceuticals.

Secondly, we identify growth regions. Specific things are made in specific parts of the world. Some parts of the world have less potential than others, and we also factor in the political and currency exposure. This is obviously personal preference. For example, I am not too convinced on the growth of the British economy post-Brexit, considering they are losing access to the Common Market, with no viable replacement. For example, the nearly 40 million unemployed in the US means we need to consider the market with caution. It would take a massive restructuring of the US economy to fix that; it is no longer a case of simply opening the economy.

Finally, we look a all these factors, and consider where the market will be in a decade or fifteen years from now. This also means considering currency exposure. One of the considerations is also lifestyle changes in a post-pandemic economy. This means shorter supply chains, less emphasis on just in time, and a decline in the retail sector. People are used to having things delivered to their doorstep. It would take a very good reason for crowds to throng malls.

In all this, it is important to be diversified, across industries, markets, and demographics. It is a foolish investor who puts all his eggs in one basket, no matter how bullish he is on any company or country. Investment should be divested from sentiment. This diversification protects against market volatility and inflation, since there is always growth somewhere.

When it comes to entering the market, it is best to use strategies such as dollar cost averaging, instead of trying to time the market. Most people who time the market fail. Unless you have supercomputers, teams of analysts and algorithms, the average investor will fail. Investing is a science not superstition. This allows us to ride the volatility of the market. Ultimately, it is time that allows our investments to grow.

Terence Kenneth John Nunis

[Shared with permission from: https://terencenunisconsulting.blogspot.com/2020/05/investing-in-volatile-market.html?m=1 ]

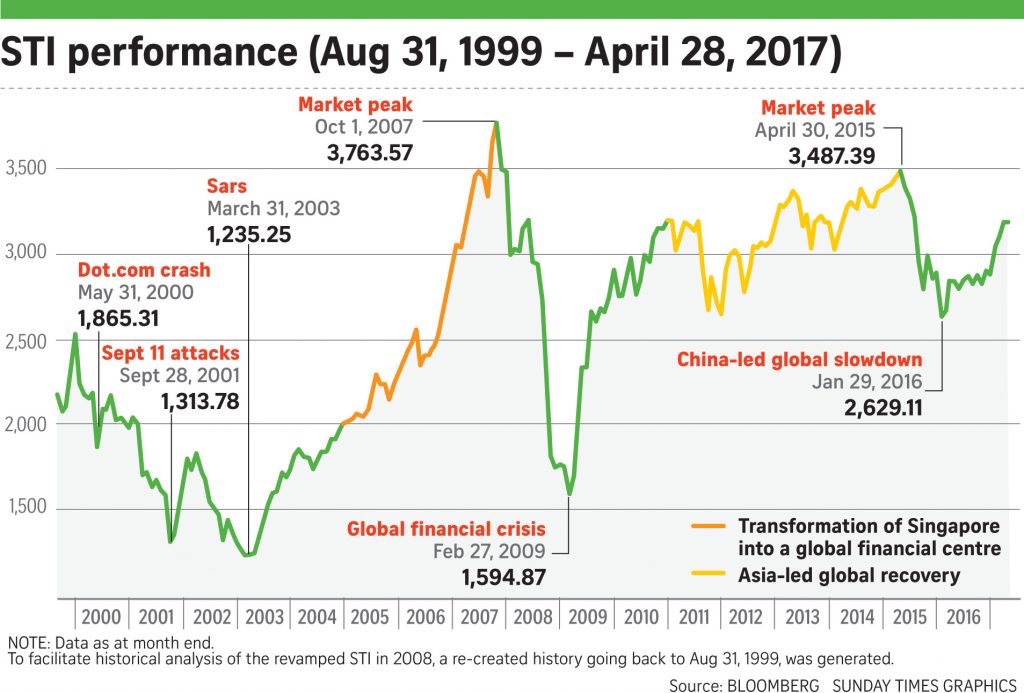

Image source: As the Straits Times Index turns 50, three experts weigh in and offer tips for investors

3 key takeaways:

- Investing over an extended investment horizon works

- Identify growth industries and growth regions

- Use strategies like Dollar-cost averaging, instead of timing the market

I’ve listened to Aberdeen Standard Investments market and funds update earlier. And will be listening in to First Eagle Amundi market and fund update on Tuesday.

After which, I’ll share some additional thoughts.